The classification of goods under the Harmonized System (HS) of Nomenclature is critical for determining the correct duty and tax rates on imports. M/s Samsung India Electronics Pvt. Ltd. faced a significant tariff dispute regarding the classification of imported IC-Codecs. This case highlights the complexities of HS classification, technical interpretation of products, and the role of appellate tribunals in resolving such disputes.

Background

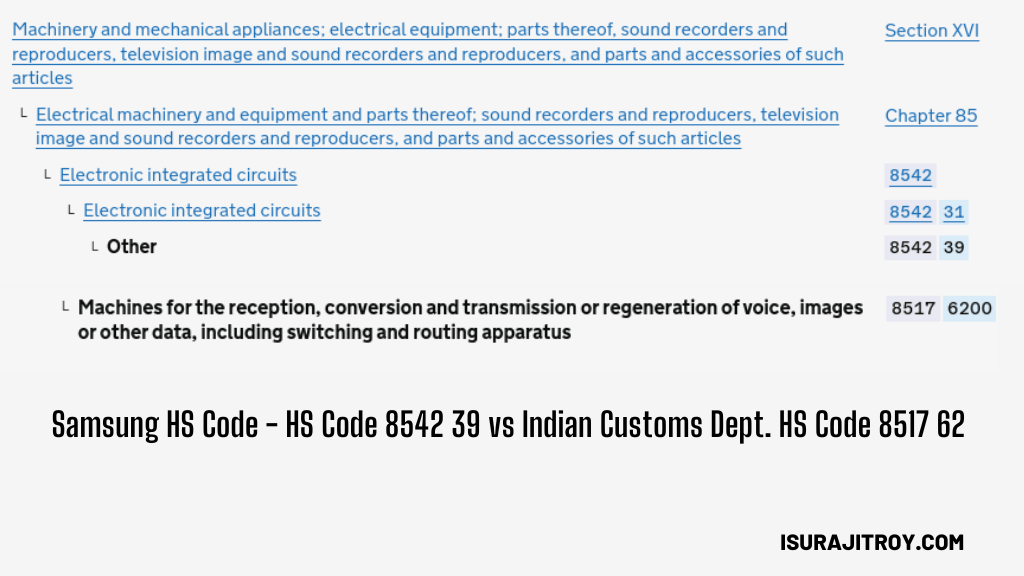

M/s Samsung India Electronics Pvt. Ltd., a leading manufacturer of mobile phones and tablets, imported IC-Codecs (Integrated Circuits) during March 2018 to March 2019. The company classified these imports under HS Code 8542 39 00, claiming they were electronic integrated circuits. This classification entitled the company to a concessional duty rate of 7.5% and an IGST rate of 12%, per a government notification.

However, the Customs Department reclassified the IC-Codecs under HS Code 8517 62 90 (communication apparatus), which attracted a higher customs duty rate of 10% and an IGST rate of 18%. Consequently, the department raised a demand for differential duty amounting to ₹1.89 crore. This led to a prolonged legal battle that culminated in an appeal before the Customs, Excise & Service Tax Appellate Tribunal (CESTAT).

Key Issues

1. Classification Dispute:

- Samsung’s Claim: IC-Codecs are classified as electronic integrated circuits under HS Code 8542 39 00, which does not encompass communication devices.

- Customs Department’s Stand: IC-Codecs fall under HS Code 8517 62 90 as “other communication apparatus,” as they have the capability for data transmission and reception when integrated with other components.

2. Technical Features of IC-Codecs:

- The IC-Codecs imported by Samsung are monolithic integrated circuits with digital signal processors (DSPs), general-purpose input/output (GPIO) pins, and Inter-Integrated Circuit (I2C) interfaces.

- These circuits require mounting on printed circuit boards (PCBs) and external power supply to become functional. At the time of import, they cannot independently transmit or receive data.

3. Applicability of Tariff Rules:

- The Customs Department invoked Section Note 3 to Section XVI and argued that components used in mobile phones must be classified as parts of communication devices.

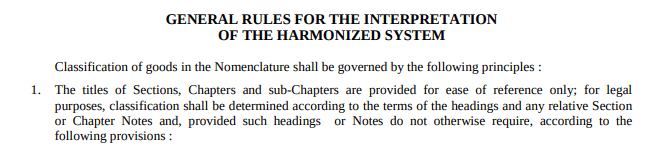

- Samsung argued that under Rule 1 of the General Rules for Interpretation, goods must be classified according to their essential characteristics at the time of import.

4. Revenue Neutrality:

- Samsung contended that even if classified under HS Code 8517, the IGST paid on import could be credited, making the demand for differential duty revenue-neutral.

Tribunal’s Findings

- Nature of Goods: The tribunal confirmed that IC-Codecs, at the time of import, are electronic integrated circuits without independent transmission or reception capabilities. It rejected the department’s claim that these circuits qualify as “communication apparatus” under HS Code 8517.

- Applicability of HS Code 8542: HS Code 8542 specifically covers electronic integrated circuits, including monolithic integrated circuits like IC-Codecs. Chapter Note 9(b) to Chapter 85 provides that such circuits, even in un-diced wafer form, are classifiable under this heading. The tribunal found Samsung’s classification under HS Code 8542 39 00 appropriate and in compliance with the General Rules for Interpretation.

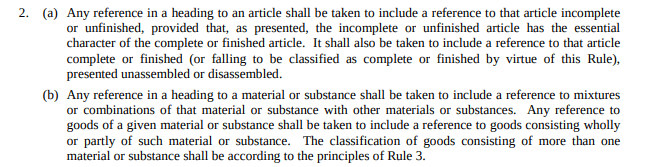

- Department’s Arguments Refuted: The tribunal noted that the Customs Department failed to provide technical evidence to support its reclassification under HS Code 8517. It also dismissed the relevance of Rule 2(b) (classification of mixtures) as IC-Codecs are not mixtures or combinations of materials.

- Revenue Neutrality and Exemption: The tribunal acknowledged that even under HS Code 8517, the IGST paid by Samsung would be creditable, reducing the practical impact on revenue. It also upheld Samsung’s entitlement to the duty exemption under the 2005 notification for goods under HS Code 8542.

- No Confiscation or Penalty: The tribunal upheld the Principal Commissioner’s decision not to impose penalties or confiscate the goods under Section 111(m) and 112(a)(ii) of the Customs Act, citing lack of malintent.

Final Judgment

The tribunal issued the following orders:

1. Allowed Customs Appeal No. 51172 of 2020, filed by Samsung, affirming the classification of IC-Codecs under HS Code 8542 39 00.

2. Dismissed Customs Appeal No. 51204 of 2020, filed by the department, challenging the Principal Commissioner’s decision to refrain from confiscating the goods and imposing penalties.

Analysis and Implications

- Legal Precedence: This case sets a precedent for future disputes involving electronic components, emphasizing the need to evaluate goods based on their technical characteristics at the time of import.

- Role of Technical Evidence: Accurate technical documentation was pivotal for Samsung in proving that IC-Codecs are integrated circuits rather than communication apparatus. This highlights the importance of aligning product descriptions with tariff classifications.

- Revenue Neutrality: By highlighting the revenue-neutral nature of the dispute, Samsung undermined the department’s justification for the demand.

- Challenges in HS Classification: The case illustrates the complexities of HS classification, especially for advanced electronic goods. It underscores the need for clarity in tariff schedules and explanatory notes to reduce ambiguity.

- Impact on Industry: Favorable rulings in such cases provide relief to import-dependent industries by preventing arbitrary tariff reclassifications that increase costs.

Conclusion

The HS code and tariff dispute involving M/s Samsung India Electronics Pvt. Ltd. showcases the intricacies of customs classification, the importance of adhering to established legal principles, and the role of appellate tribunals in resolving such conflicts. The tribunal’s decision underscores the need for precise classification based on the inherent characteristics of goods at the time of import. It also highlights the significance of thorough documentation and technical clarity in defending classification disputes.

This case not only safeguards the interests of the appellant but also provides guidance for businesses and customs authorities on resolving similar issues in the future.