Citation: 2026 INSC 19 · Civil Appeal No. 5531 of 2025 · Supreme Court of India · Decided 06 January 2026 · Bench: J.B. Pardiwala & R. Mahadevan, JJ.

The question in one line: Are aluminium shelves imported for mushroom growing “aluminium structures” of Chapter 76, or “parts of agricultural machinery” of Chapter 84?

Scope note. This study analyses the classification reasoning at the WCO Harmonized System 6-digit level, grounded in the General Interpretative Rules (GRI 1–6, 2022 edition) and the WCO Explanatory Notes. It is educational commentary, not

a binding ruling. National tariff items beyond six digits (the Indian 8-digit CTI) are referenced only as they appear in the judgment.

At a Glance

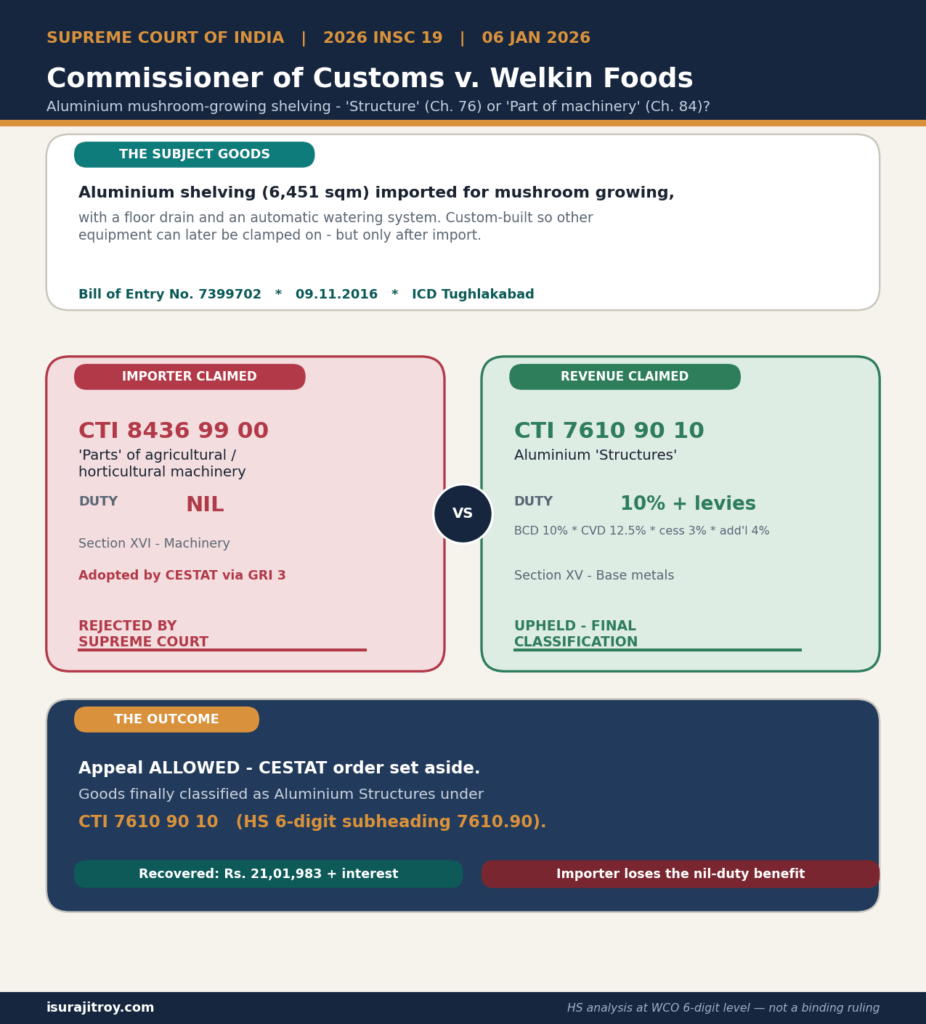

Figure 1 — Case at a glance.

A single phrase captures the holding: the Supreme Court restored the Revenue’s classification, holding the shelving to be aluminium structures under CTI 7610 90 10 (HS subheading 7610.90), reversing CESTAT. The importer lost the nil-duty benefit it had claimed under CTI 8436 99 00, and the short-levied duty of ₹21,01,983 (plus interest) became recoverable under Section 28 of the Customs Act, 1962.

Factual Matrix

M/s Welkin Foods imported aluminium shelving (6,451.20 sqm), together with a floor drain and an automatic watering system, under Bill of Entry No. 7399702 dated 09.11.2016 at ICD Tughlakabad. All three items were declared under CTI 8436 99 00 — parts of agricultural/horticultural machinery — which carries a nil rate of duty.

The Revenue accepted the floor drain and watering system under 8436 99 00, but on audit took the view that the shelving was an aluminium structure properly classifiable under CTI 7610 90 10, attracting basic customs duty of 10% along with countervailing duty (12.5%), customs cess (3%) and additional customs duty (4%). A show-cause notice followed, alleging a short levy of ₹21,01,983 recoverable under Section 28(1) with interest under Section 28AA.

The shelves were custom-built so that the other mushroom-cultivation equipment — head-filling machines, the watering system, compost-spreading and spraying equipment — could be clamped onto them after importation. At the time of import, however, the shelving was simply aluminium shelving.

Issue to Be Determined

Whether the subject goods are classifiable as ‘parts’ of machines / mechanical appliances of Chapter 84 under CTI 8436 99 00, or as aluminium structures of Chapter 76 under CTI 7610 90 10.

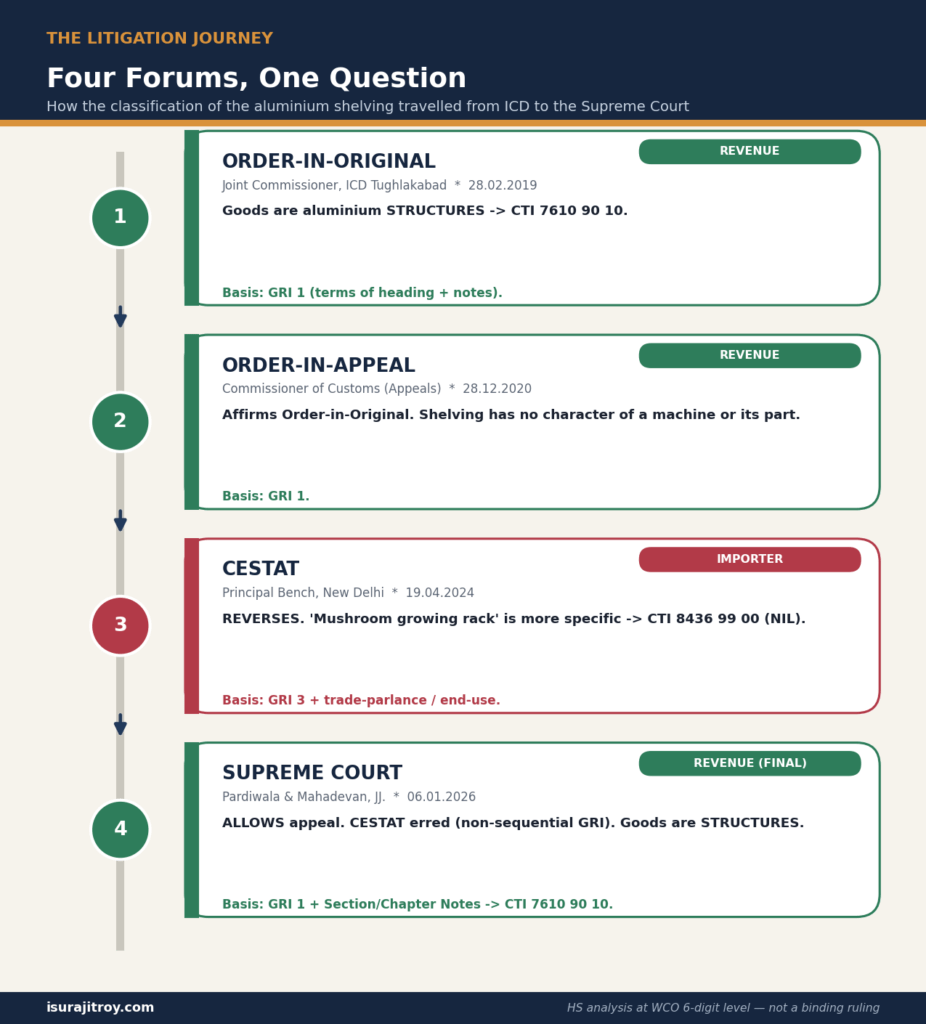

The Litigation Journey

Figure 2 — Four forums, one question.

| Forum | Date | Outcome | Decisive basis |

| Order-in-Original (Joint Commr., ICD TKD) | 28.02.2019 | Goods are structures → 7610 90 10 | GRI 1 (terms of heading + Notes) |

| Order-in-Appeal (Commr. Appeals) | 28.12.2020 | Affirms Order-in-Original | GRI 1 |

| CESTAT (Principal Bench, New Delhi) | 19.04.2024 | Reverses → 8436 99 00 (nil) | GRI 3 + trade-parlance / end-use |

| Supreme Court | 06.01.2026 | Allows appeal → 7610 90 10 | GRI 1 + Section / Chapter Notes |

The pendulum swung once: the two departmental authorities and the Supreme Court agreed (structures); CESTAT alone went the other way. The reason CESTAT’s order could not survive is methodological — it applied the GRIs out of sequence.

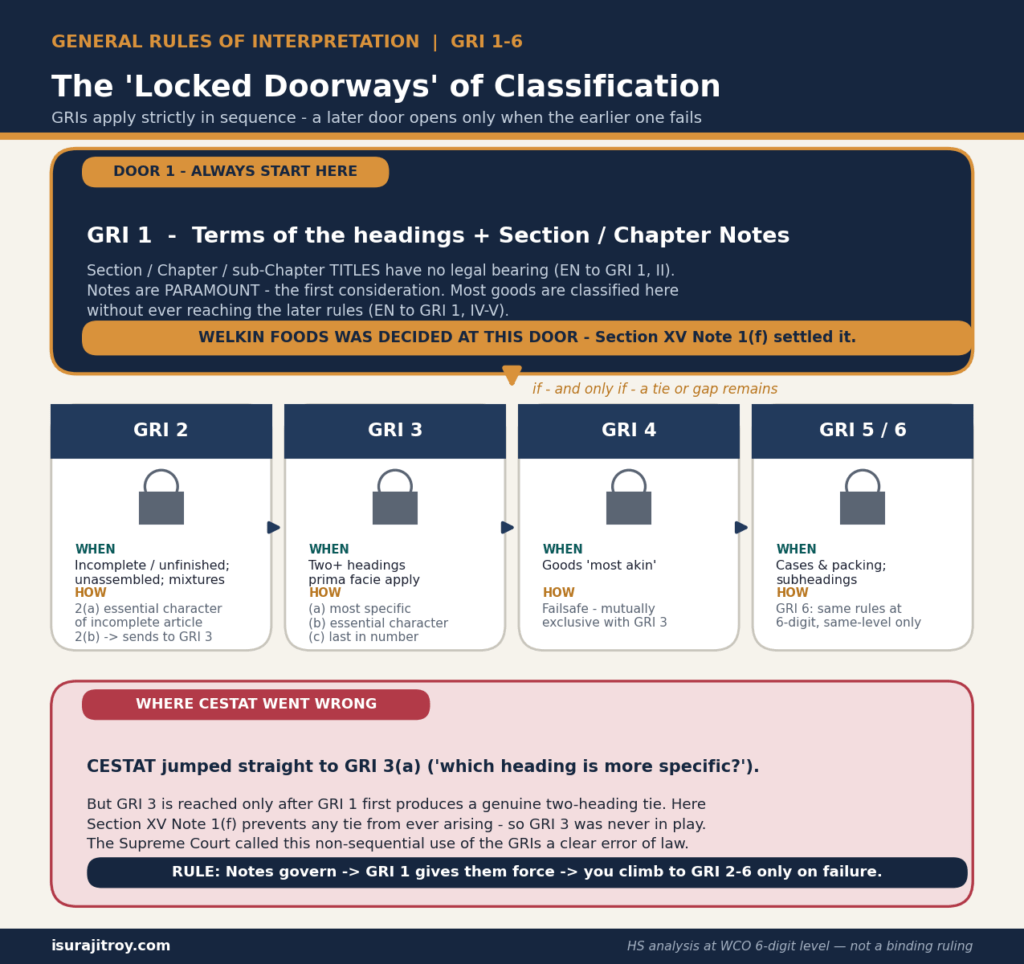

The Interpretative Framework

1. GRI 1 governs; later rules are “locked doorways”

Figure 3 — The ‘locked doorways’ of classification.

GRI 1 provides that classification is determined “according to the terms of the headings and any relative Section or Chapter Notes.” The Explanatory Notes to GRI 1 add two points the Court leaned on heavily:

- Section, Chapter and sub-Chapter titles are “for ease of reference only” and have no legal bearing (EN to GRI 1, paragraph II).

- The headings and relative Notes are paramount — the first consideration — and a great many goods are classified on GRI 1 alone, without recourse to the later rules (EN to GRI 1, paragraphs IV–V).

The Court adopted a “locked doorways” image: classification begins, and usually ends, at GRI 1. GRI 2–5 are reached only when GRI 1 (with the Notes) fails to resolve the matter; GRI 3, in particular, can be reached only once GRI 1 produces a genuine tie between two or more headings; and GRI 6 (the same rules applied mutatis mutandis at subheading level, comparing only subheadings at the same dash-level) comes last.

This sequencing is the spine of the judgment. CESTAT’s error was to walk straight to GRI 3(a) and ask which heading was “more specific,” without first establishing — under GRI 1 — that the goods were even prima facie classifiable under both competing headings.

2. Two supporting doctrines (applied with restraint)

The judgment also restates two recurring tools, but is careful to subordinate both to GRI 1:

- Common / trade parlance test — invoked only in the absence of statutory guidance, where the heading uses no scientific/technical term and the result would not contradict the statutory scheme. It cannot reclassify goods that are clearly identifiable under a heading merely because the trade calls them by a different name.

- ‘Use’ vs. ‘eo-nomine’ — use may be considered only where the heading refers to use or adaptation, explicitly or inherently; and then only the intended use discernible from the goods’ objective characteristics at the time of import (the as-imported principle), not the actual or subjective end use.

Both doctrines pointed the same way here, but neither was needed to decide the case — the Notes did that.

The Competing Headings and Their Notes

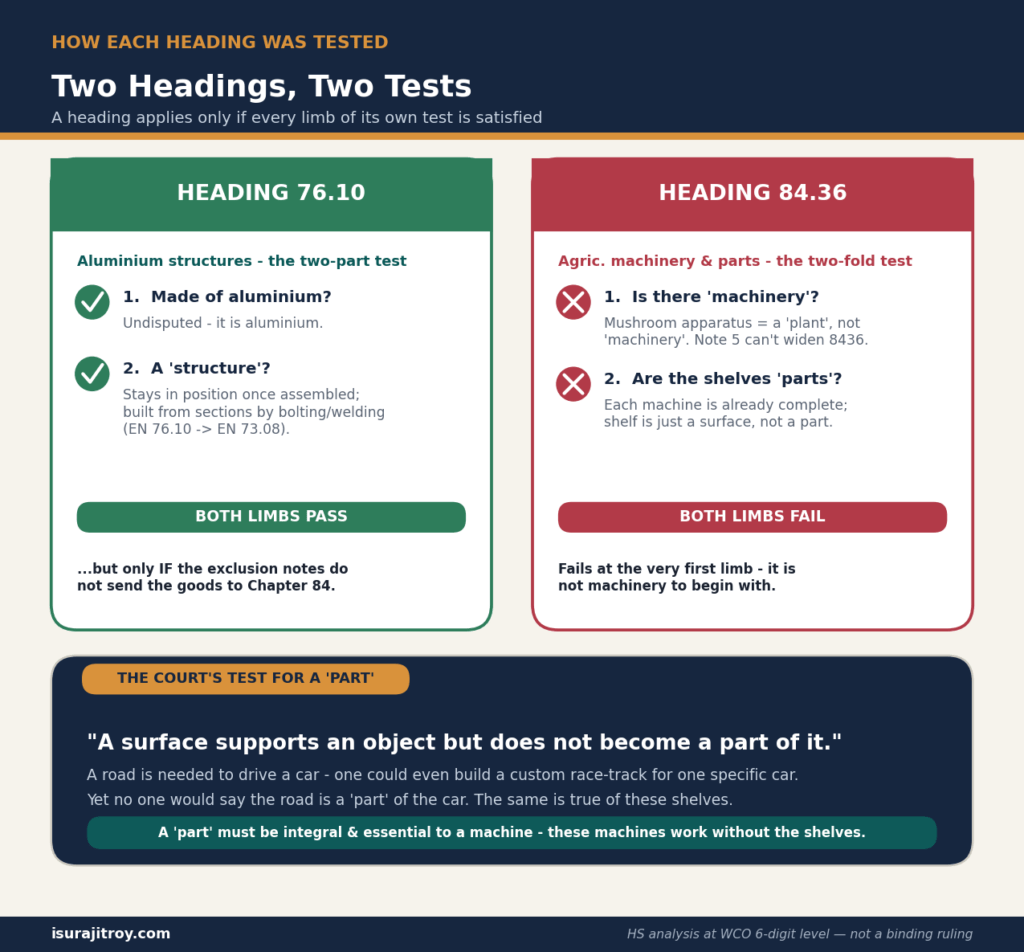

Figure 4 — Two headings, two tests.

1. Heading 76.10 — Aluminium structures

76.10 — Aluminium structures (excluding prefabricated buildings of heading 94.06) and parts of structures … ; aluminium plates, rods, profiles, tubes and the like, prepared for use in structures. One-dash subheadings: 7610.10 (doors, windows and their frames and thresholds for doors) · 7610.90 (Other).

Two-part test for 76.10: the goods must (1) be of aluminium, and (2) be a structure (or part of one). The first limb was undisputed. For the second, the Nomenclature gives no definition, but the EN to 76.10 directs that the EN to heading 73.08 applies mutatis mutandis. The EN to 73.08 supplies the working criterion of a “structure”:

- once put in position, the article generally remains in that position; and

- it is usually built up from bars, rods, tubes, sections, sheets, plates, etc., by riveting, bolting, welding and the like.

Tellingly, that same EN expressly lists, among the goods of the heading, “large-scale shelving for assembly and permanent installation in shops, workshops, storehouses … stalls and racks.” Shelving and racks are textbook structures. On its objective characteristics, the shelving fits the heading.

2. Heading 84.36 — Agricultural machinery and parts

84.36 — Other agricultural, horticultural, forestry, poultry-keeping or bee-keeping machinery … ; poultry incubators and brooders. “– Parts:” → 8436.91 (of poultry-keeping machinery / incubators and brooders) · 8436.99 (Other). The importer claimed 8436 99 00.

Two-fold test for 84.36 (parts): there must first be (1) agricultural machinery, and (2) the subject goods must be parts of that machinery. The relevant governing Notes are:

- Section XVI, Note 2 — the parts-classification rules (parts that are themselves goods of a Chapter 84/85 heading go to their own heading; other parts suitable for use solely or principally with a particular machine go with that machine).

- Section XVI, Note 3 — composite machines and multi-function machines are classified by their principal function.

- Section XVI, Note 4 — functional units: separate components intended to contribute together to a single clearly-defined function are classified by that function.

- Section XVI, Note 5 — for the purposes of these Notes, “machine” means any machine, machinery, plant, equipment, apparatus or appliance cited in the headings of Chapter 84 or 85.

- Chapter 84, Note 7 — a machine used for more than one purpose is treated as if its principal purpose were its sole purpose.

- EN to Chapter 84 — headings 84.25 to 84.78 (which include 84.36) group machines by the field of industry in which they are used.

So 84.36 is an eo-nomine heading for “machinery” that inherently imports a principal-use test (“agricultural”). But the eo-nomine core — machinery — must be satisfied first.

3. The exclusion link that makes the contest decisive

Two Notes ensure the two headings cannot both apply:

- Section XV, Note 1(f) — Section XV (which houses Chapter 76) does not cover articles of Section XVI (machinery, mechanical appliances and electrical goods).

- EN to 76.10(a) — the heading excludes “assemblies identifiable as parts of articles of Chapters 84 to 88.”

The effect: if the shelving genuinely qualifies as a part of agricultural machinery under Chapter 84, it is barred from 76.10. Conversely, if it does not so qualify, the bar never operates and it remains in 76.10. The whole case therefore collapses into a single GRI 1 inquiry into Heading 84.36 — no tie, no GRI 3.

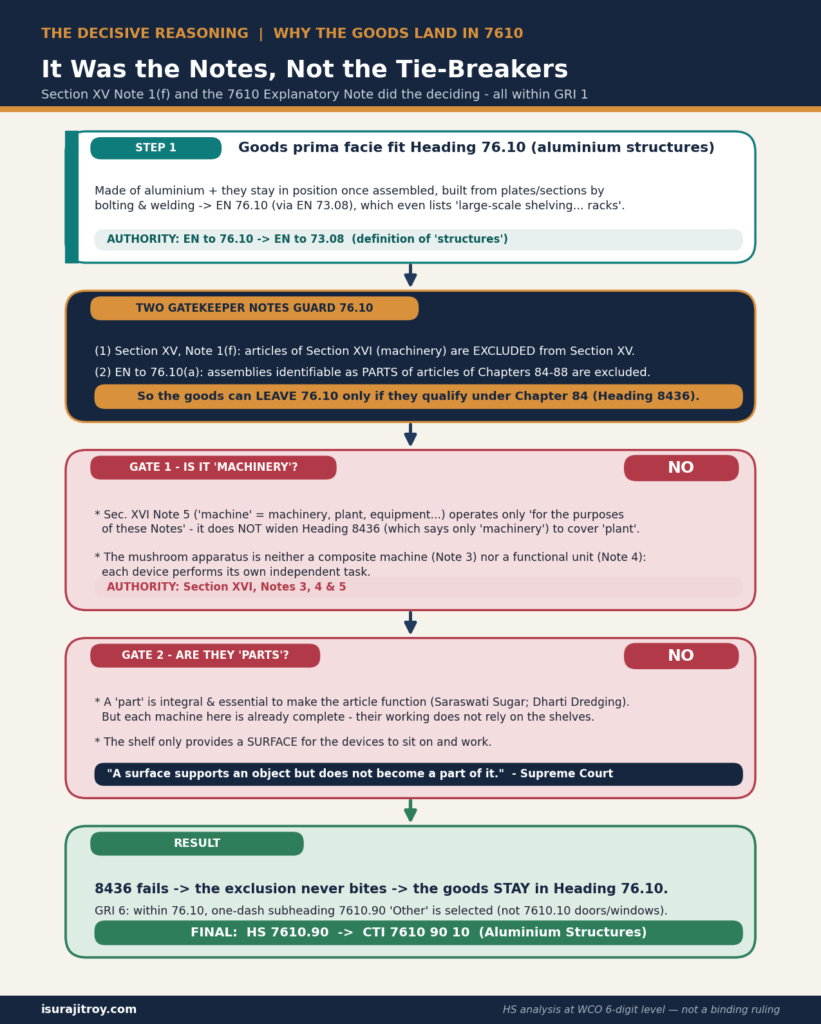

The Court’s Reasoning — Why 7610 Wins

Figure 5 — It was the Notes, not the tie-breakers.

Step 1 — The shelving prima facie answers Heading 76.10. Applying the EN to 76.10 (through the EN to 73.08), the goods are aluminium, remain in position once installed, and are built up by bolting/welding — the very profile of a structure, and indeed of the “shelving … racks” the EN names.

Step 2 — The gatekeeper Notes. Section XV Note 1(f) and EN 76.10(a) mean the goods can leave 76.10 only by qualifying under Chapter 84. So the Court tested Heading 84.36.

Gate 1 — Is there “machinery”? No.

- The respondent leaned on Section XVI Note 5 to argue that “machine” embraces “plant,” so a mushroom-growing plant qualifies. The Court read Note 5 strictly: its umbrella definition operates “for the purposes of these Notes” only — it does not widen Heading 84.36, whose text says simply “machinery.” A heading that names only “machinery” cannot be stretched to “plant”; where the legislature wanted “plant,” it said so (e.g., headings 84.04, 84.19). The deliberate inclusion of “germination plant” in 84.36 confirms that other “plants” are not otherwise covered.

- The “mushroom growing apparatus” was, at best, a collection of independent machines. It was not a composite machine (Note 3) — the machines are not fitted together to form a permanent whole — and not a functional unit (Note 4) — each device (head-filling, watering, compost-spreading) performs its own independent task rather than contributing to one clearly-defined function. By the EN’s own examples (an integrated irrigation system is a functional unit; a CCTV assembly is not), the apparatus falls on the wrong side of the line.

- In plain terms, a static, non-moving aluminium shelf is understood as a structure or furniture — not as a machine.

Gate 2 — Are the shelves “parts”? No. Even assuming machinery existed, a part (per Saraswati Sugar Mills and Dharti Dredging) is an integral, essential component without which the article cannot function. Here every machine clamped onto the shelving is already complete and self-contained; their mechanical and electrical operation does not depend on the shelves. The shelving merely furnishes a surface. The Court’s memorable formulation:

“A surface supports an object but does not become a part of it.”

— illustrated by the analogy that a car needs a road (one might even build a bespoke race-track for one car), yet no one calls the road a “part” of the car.

Result. Heading 84.36 fails at both limbs; the exclusion Notes never bite; the goods remain in 76.10. Applying GRI 6, within 76.10 the one-dash subheading 7610.90 (“Other”) is the correct level (the goods are not doors/windows of 7610.10), yielding HS 7610.90 and, in the Indian schedule, CTI 7610 90 10.

Why CESTAT’s order fell. Two flaws: (i) it invoked GRI 3(a) (“more specific heading”) without a GRI 1 tie — a non-sequential, impermissible use of the rules, made worse because Section XV Note 1(f) would itself have resolved any overlap; and (ii) it rested “no other purpose” and “trade parlance” findings on a brochure and the supplier’s identity, without the rigorous, objective, design-based evidence the law demands to give goods a separate commercial identity.

Holding and Final Classification

| Element | Determination |

| Heading | 76.10 — Aluminium structures … and parts of structures … prepared for use in structures |

| One-dash subheading (GRI 6) | 7610.90 — Other (not 7610.10 doors/windows) |

| HS 6-digit code | 7610.90 |

| Indian Customs Tariff Item | 7610 90 10 — Structures |

| Heading 84.36 / CTI 8436 99 00 | Rejected — goods are neither “machinery” nor “parts” of machinery |

| Disposition | Appeal allowed; CESTAT Final Order dated 19.04.2024 set aside |

| Revenue effect | Short-levied duty ₹21,01,983 + interest recoverable (Sec. 28 / 28AA, Customs Act 1962); importer loses the nil-duty benefit |

Practitioner Takeaways

- GRIs are a sequence, not a menu. Never reach for GRI 3(a)’s “most specific heading” until GRI 1 has actually produced a two-heading tie. Skipping straight to “specificity” is the single error that sank the CESTAT order.

- A Section/Chapter Note that excludes can decide the whole case. Section XV Note 1(f) (and the parallel EN 76.10 exclusion) made the dispute a one-heading inquiry. Always check exclusion Notes before arguing specificity.

- “Machinery” means machinery. Section XVI Note 5’s umbrella (“plant, equipment, apparatus, appliance”) operates only inside the Section Notes; it does not enlarge a heading whose text says only “machinery.”

- Composite machine ≠ functional unit ≠ a loose assembly. Test Notes 3 and 4 against the facts: permanent fitting-together, or one clearly-defined function. Independent machines doing separate tasks are neither.

- “Part” has a high threshold. It must be integral and essential to the article’s function. A mounting surface, base, or platform that the machine does not depend on is not a part.

- Classify the goods as imported. End use matters only where the heading invites it (explicitly or inherently) and only as intended use evident from the goods’ objective characteristics — never the importer’s stated future plans or brochures.

- Separate commercial identity must be proven, not asserted. A trade name (“mushroom growing rack”) backed only by marketing material and supplier identity does not displace a clear statutory description.

Authorities Index (Notes & Rules Relied On)

| Instrument | Use in the case |

| GRI 1 (+ EN paras II, IV, V) | Primacy of headings and Notes; titles have no legal bearing; sequencing |

| GRI 3 (+ EN) | Reached only on a genuine tie; CESTAT’s misuse identified |

| GRI 6 (+ EN) | Descent to one-dash subheading 7610.90; same-level comparison |

| Section XV, Note 1(f) | Excludes Section XVI machinery from Section XV — the pivotal exclusion |

| EN to heading 76.10 | “Structure” criterion via EN 73.08; exclusion of Ch. 84–88 parts |

| EN to heading 73.08 | Definition of structures; expressly lists “shelving … stalls and racks” |

| Section XVI, Notes 2, 3, 4, 5 | Parts rules; composite machine; functional unit; “machine” umbrella |

| Chapter 84, Note 7 | Principal-purpose rule for multi-purpose machines |

| EN to Chapter 84 | Headings 84.25–84.78 grouped by field of industry |

| Saraswati Sugar Mills (2014) 15 SCC 625; Dharti Dredging (2023) 18 SCC 103 | Test for “part” — integral and essential to function |

Caveats

- This analysis operates at the WCO 6-digit level (HS 2022). The decision turns on Notes that are identical in the Indian First Schedule and the HSN, so the Explanatory Notes were treated as binding guidance (per Madhan Agro); where a national schedule deviates from the HSN, that alignment must be re-checked.

- The Indian 8-digit CTI (7610 90 10) is a national sub-division below the harmonized 6-digit code 7610.90 and is reproduced only as it features in the judgment.

- The outcome is fact-sensitive. Had the assembly satisfied the functional-unit test (Note 4), or had the shelving been an integral, function-bearing component rather than a mere surface, the analysis at Gates 1–2 could have differed.

- Educational commentary only; not a binding tariff ruling, which only the customs authority can issue.